ITR Forms AY2026-27

Quick Summary of ITR Forms for AY 2026-27

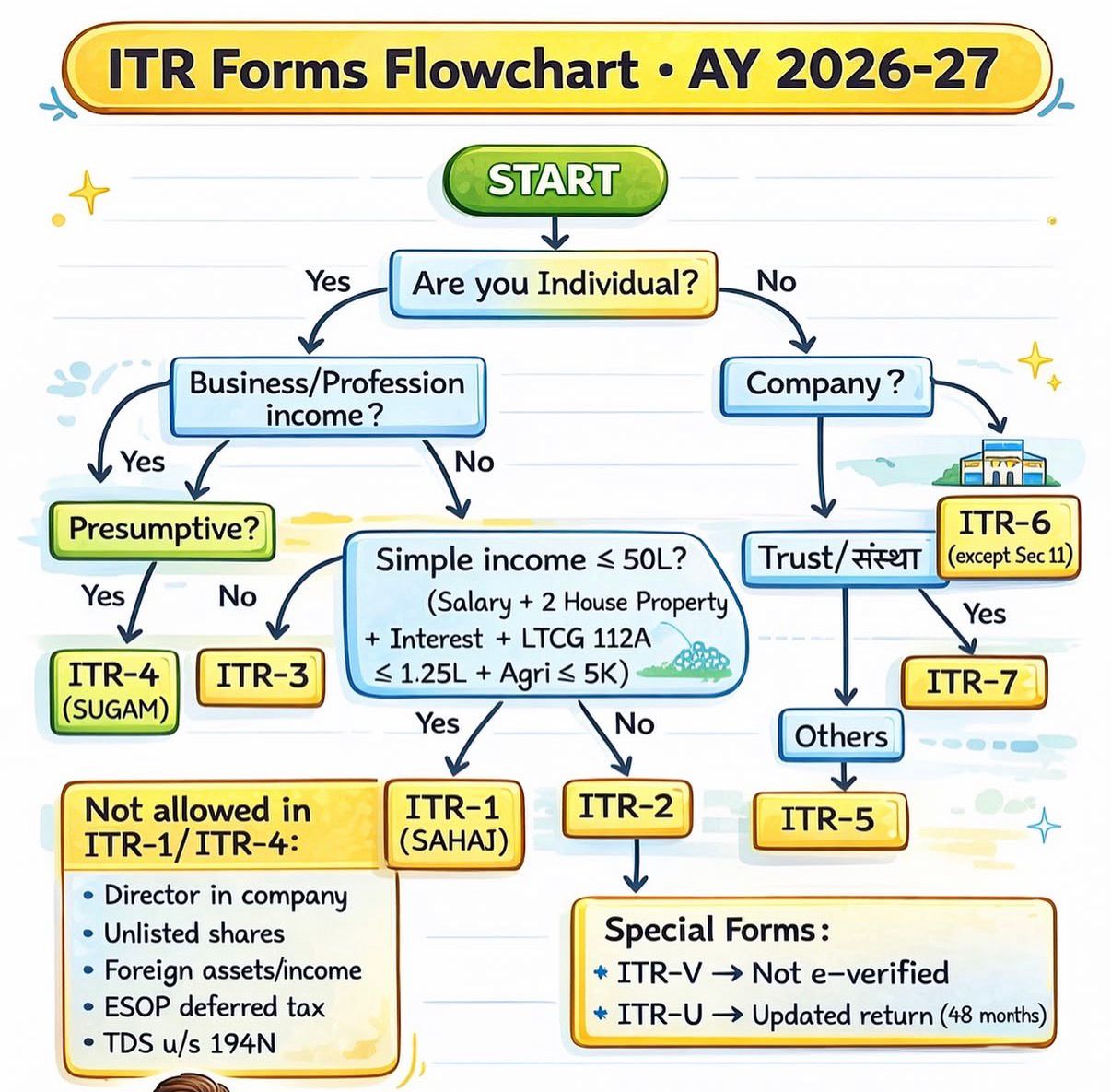

For Assessment Year (AY) 2026-27, the Income Tax Department has released updated ITR forms. Understanding which form to use is primarily determined by your source of income, residential status, and total income level.

| ITR Form | Primary Eligibility |

| ITR-1 (Sahaj) | Residents with income up to ₹50 Lakh from Salary/Pension, one house property, and "Other Sources." Includes limited reporting for Long-Term Capital Gains (LTCG) up to ₹1.25 lakh. |

| ITR-2 | Individuals/HUFs not having income from business or profession. Used for capital gains, multiple house properties, foreign assets, or when ineligible for ITR-1. |

| ITR-3 | Individuals/HUFs with income from a proprietary business or profession. Also for those who are partners in a firm. |

| ITR-4 (Sugam) | Residents, HUFs, and firms (excluding LLPs) opting for the presumptive taxation scheme (Sec 44AD, 44ADA, 44AE) with income up to ₹50 Lakh. |

| ITR-5 | LLPs, partnership firms, AOPs, BOIs, and other non-individual entities. |

| ITR-6 | Companies (excluding those claiming Section 11 exemption). |

| ITR-7 | Trusts, political parties, research institutions, and similar entities. |

Quick Summary of ITR Forms for AY 2026-27

| Taxpayer Category | Due Date |

| Non-Audit Cases (ITR-1, ITR-2) | July 31, 2026 |

| Non-Audit Cases (ITR-3, ITR-4) | August 31, 2026 |

| Audit Cases (All ITRs) | October 31, 2026 |

| Transfer Pricing Cases (Form 3CEB) | November 30, 2026 |

Key Compliance Updates for AY 2026-27

Several specific disclosure requirements have been introduced this year that affect how income must be classified.

-

Reporting of NBFC/HFC Interest Income: A significant change for this year is the explicit requirement to declare interest earned from Non-Banking Financial Companies (NBFCs), Housing Finance Companies (HFCs), and corporate debentures under the "Others" column of Schedule OS. This removes previous ambiguities and requires precise reporting for clients with investment portfolios.

Need help with this? Talk to Rongmei Fintech and Financial Solution → -

Updated Forms & Utility: The Income Tax Department has released the updated ITR-U (for updated returns) and ITR-V forms. The ITR-U form, which allows for the correction of past filings, now includes a revised Part B ATI computation column to address specific tax liabilities if filing in response to a notice issued under Section 148.

-

New Legislation Context: Please note that while the Income Tax Act, 2025 is effective from April 1, 2026, it applies primarily to the Tax Year 2026-27 onwards (income earned from April 1, 2026). The filing for AY 2026-27 (FY 2025-26) remains governed by the established regulatory framework. However, familiarizing your team with the new forms and structural changes under the new Act is advisable for future-proofing your advisory services.

Key Updates and Changes for AY 2026-27

-

ITR-1 Adjustments: You can now report LTCG under section 112A (up to ₹1.25 lakh) in ITR-1, provided there are no brought-forward losses.

Need help with this? Talk to Rongmei Fintech and Financial Solution → -

Tax Regime: The "New Tax Regime" remains the default. To opt for the "Old Tax Regime," taxpayers with business/professional income must furnish Form 10-IEA on or before the due date.

-

Aadhaar: Only valid 12-digit Aadhaar numbers are accepted; the 28-digit Enrolment ID is no longer valid.

Important Deadlines

-

Non-Audit Cases: July 31, 2026.

Need help with this? Talk to Rongmei Fintech and Financial Solution → -

Audit Cases (ITR-3): October 31, 2026.

Have Questions? We're Here to Help

Get expert advice from Rongmei Fintech and Financial Solution. Reach out to discuss your requirements.